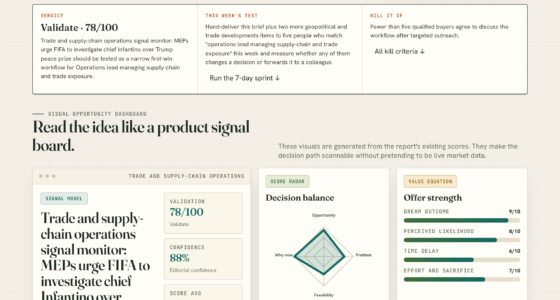

📊 Full opportunity report: The $60 Billion Bargain: Why Cursor Could Be a Steal for SpaceX on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

SpaceX acquired Cursor, an AI coding toolmaker, for $60 billion in stock, a deal that appears highly advantageous given Cursor’s rapid revenue growth and strategic assets. This move signals a major shift in AI integration within aerospace and tech sectors.

SpaceX announced on June 16 that it will acquire Cursor, the AI coding platform, for $60 billion in all-stock. This strategic move, made just days after SpaceX’s historic IPO valuation exceeding $2 trillion, positions the aerospace giant to capitalize on AI-driven software tools in a way that could influence both tech and space industries.

The acquisition was executed entirely with SpaceX stock, representing only about 3.4% dilution at the IPO valuation. Immediately following the announcement, SpaceX’s stock surged approximately 16%, boosting its market cap to nearly $2.94 trillion and briefly surpassing Microsoft and Amazon in valuation. Cursor, which reported roughly $4 billion in annualized revenue at the time, has experienced rapid growth, doubling its revenue from February to June 2024 and projecting over $6 billion by the end of 2026. The deal values Cursor at a forward multiple of about 10x revenue, which is considered favorable in AI industry standards, especially given its growth trajectory.

Cursor’s assets include a large user base of over 1 million paying users and 50,000 enterprise clients, with a profitable enterprise subscription segment. It also developed its own coding model, Composer, which performs the majority of its AI work, and has rebuffed offers from major players like OpenAI and Microsoft, indicating its strategic independence and value.

The $60B bargain: why Cursor could be a steal

$60 billion for a code editor sounds like a bubble. Look past the headline and the price isn’t the scandal — it’s the discount. Here’s the case that SpaceX got Cursor cheap.

A melting multiple, paid in appreciating paper that cost almost nothing, for the profitable leader of the only AI category reliably making money — plus the missing app layer and an escape from the margin trap. If the growth holds and integration doesn’t break the product, $60B will read like a down payment. The risk isn’t overpaying for what Cursor is — it’s breaking what made it worth buying.

Strategic Impact of the Cursor Acquisition for SpaceX

This acquisition provides SpaceX with a profitable foothold in AI software, a sector increasingly vital for automation, software development, and enterprise workflows. By owning Cursor’s technology and team, SpaceX gains a distribution gateway into enterprise AI markets, potentially influencing future aerospace and tech innovations. The deal also offers a path to significantly reduce costs by integrating AI models and infrastructure in-house, moving away from costly third-party API fees, and establishing vertical integration that aligns with Elon Musk’s proven strategy of building in-house capabilities.

Agentic Coding with Claude Code: The everyday developer's guide to agentic coding with Claude Code

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Background on SpaceX’s AI and Software Strategy

Prior to this deal, SpaceX primarily focused on aerospace hardware, rockets, and satellite technology. However, Elon Musk has long emphasized the importance of AI and software in future space missions and enterprise applications. Cursor, founded by Anysphere, emerged as a leading AI coding tool with rapid revenue growth and a strong enterprise presence. Its development of proprietary models and refusal to sell to major competitors made it a strategic asset. The acquisition aligns with Musk’s broader approach of acquiring and integrating advanced technology companies to build self-reliant, cost-efficient systems, as seen with Tesla, Tesla’s battery tech, and Neuralink.

“Acquiring Cursor allows us to bring AI development in-house and accelerate our technological edge in space and beyond.”

— Elon Musk, SpaceX CEO

Mastering Enterprise Platform Engineering: A practical guide to platform engineering and generative AI for high-performance software delivery

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unresolved Aspects of the Cursor Acquisition

While the deal’s financial details are confirmed, the long-term integration plans, specific use cases within SpaceX, and how Cursor’s technology will be scaled across the company’s projects remain unclear. Additionally, the impact on competitors and the AI market’s future trajectory are still developing factors, with regulatory and technological hurdles yet to be fully understood.

Mastering Cursor AI: A Step-by-Step Guide to Building with the Smartest Code Editor for Developers (AI Technology, Workflows, and Automation Book 8)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Next Steps for SpaceX and Cursor Integration

SpaceX is expected to begin integrating Cursor’s technology into its aerospace and AI workflows in the coming months. Attention will focus on how the company leverages Cursor’s models to enhance rocket automation, satellite operations, and enterprise AI services. Further announcements on product development, talent retention, and strategic partnerships are anticipated as the integration progresses.

Mastering Cursor IDE: A Practical Guide to AI-Assisted Programming and Modern Software Development

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Why did SpaceX pay such a high valuation for Cursor?

Although $60 billion seems high, it reflects Cursor’s rapid growth, strategic assets, and potential to reduce costs through vertical integration, making it a valuable long-term investment.

How will this acquisition impact SpaceX’s operations?

It is expected to enable greater AI integration in SpaceX’s projects, reduce reliance on external AI providers, and accelerate development of autonomous systems for rockets and satellites.

What does this mean for competitors in AI and aerospace?

It signals a move toward in-house AI capabilities and vertical integration, potentially challenging existing AI providers and prompting competitors to reassess their strategies.

Is this deal likely to influence AI industry valuations?

Yes, the deal’s valuation and rapid growth highlight the premium placed on AI tools with proven enterprise traction, possibly setting new benchmarks for future acquisitions.

What are the risks associated with this acquisition?

Potential risks include integration challenges, overestimation of Cursor’s long-term value, and regulatory scrutiny over AI and market dominance concerns.

Source: ThorstenMeyerAI.com